If you are running an AI company between $500K and $10M in annual revenue, you have probably already discovered that raising capital is harder than it should be. Not because your business is weak, but because the available instruments were designed for a different kind of company.

This is a practical guide to the funding options that exist today, where each one fits, and where the gaps remain.

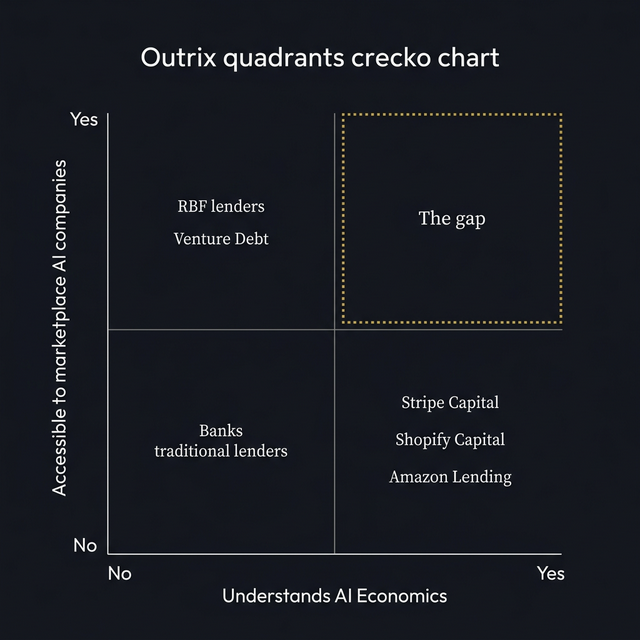

Venture equity

What it is. You sell ownership in your company to investors in exchange for capital. Typical rounds range from $1M to $20M at this stage.

Where it fits. Venture equity is appropriate when you need capital for activities with uncertain returns: hiring a sales team, building new product features, expanding into a new market. These are bets. Equity capital absorbs the risk of bets not paying off.

Where it doesn't fit. Using equity to fund working capital is one of the most expensive mistakes an AI founder can make. If you need $300,000 to cover the gap between compute costs and marketplace payouts, raising a $3M round at a $15M valuation means you gave away 20% of your company. Selling equity to solve a timing problem is like selling your house because your salary is paid monthly instead of weekly.

Revenue-based financing (RBF)

What it is. A lender advances you capital and you repay by remitting a fixed percentage of monthly revenue until a predetermined multiple is repaid. No equity dilution.

Where it fits. RBF was designed for subscription SaaS companies with predictable MRR, high gross margins, and low churn. If you run a traditional software business with 85% gross margins, RBF can be an efficient source of growth capital.

Where it doesn't fit. AI companies break the RBF model in several ways. Usage-based revenue makes monthly projections volatile. Inference costs compress margins below the thresholds most RBF lenders require (typically 60%+ gross margin).

Venture debt

What it is. A loan, typically from a specialist bank or fund, extended alongside or shortly after an equity round. Usually structured as a 2 to 4 year term loan with warrants.

Where it fits. Venture debt is designed to extend your runway between equity rounds. It works well when you have a clear path to your next raise.

Where it doesn't fit. Venture debt requires a recent venture round as a precondition. If you are bootstrapped or generate revenue without venture backing, most venture debt providers will not engage.

Traditional bank lending

What it is. A credit facility or term loan from a commercial bank, underwritten against your financial statements, assets, or personal guarantees.

Where it doesn't fit. AI startups fail nearly every criterion commercial banks use for credit decisions. No physical collateral. Short operating history. Variable revenue. Margins that look distressed by SaaS standards.

Marketplace-embedded lending

What it is. The marketplace or payment platform you already sell through offers you a cash advance, repaid automatically as a percentage of future transactions.

Where it fits. This model is elegant because the lender has real-time visibility into your revenue and can automate repayment at the transaction level.

Where it doesn't fit. These products only serve businesses operating on the lending platform's own rails. If your revenue flows through Microsoft, AWS, or Salesforce marketplaces, none of these embedded lending products can see your revenue.

What's missing

The missing product is a working capital facility that connects directly to the data sources that define your business: your inference cost APIs and your marketplace payout APIs. It would underwrite based on your receivables and revenue per dollar of compute rather than blended gross margin. It would repay by applying the full balance of incoming marketplace payouts to clear your obligations, with the residual flowing directly back to you.

Every component of this product exists in isolation. Stripe Capital proved the automated sweep repayment model. The inference cost APIs from OpenAI, Anthropic, and AWS Bedrock are accessible programmatically. The marketplace payout APIs in Partner Center and AWS Marketplace are accessible.

Nobody has assembled these components into a single product designed for AI company economics. The companies that need this product are multiplying rapidly.

Nils Hertzner | Floatcap — working capital infrastructure for AI companies.

We are building the working capital product described above: credit lines for AI companies granting up to an 80% advance rate on receivables, cleared automatically using incoming marketplace payouts. Join the waitlist.